Blogs

Trading Isn’t Binary: Moving Beyond IF–ELSE Thinking

Nick Garidzhuk

Trading Isn’t Binary: Move Beyond IF–ELSE Rules

Most platforms teach you to trade like a light switch: IF a rule fires, THEN you buy; ELSE you do nothing. Real markets aren’t that simple. They change with regime, volatility, liquidity, and headlines. This blog lays out a cleaner way to work: say what you’re trying to do (intent), read the backdrop (context), judge how well the two line up (confidence), and act accordingly (action); size up when it’s strong, scale down when it’s mixed, and wait when it isn’t there.

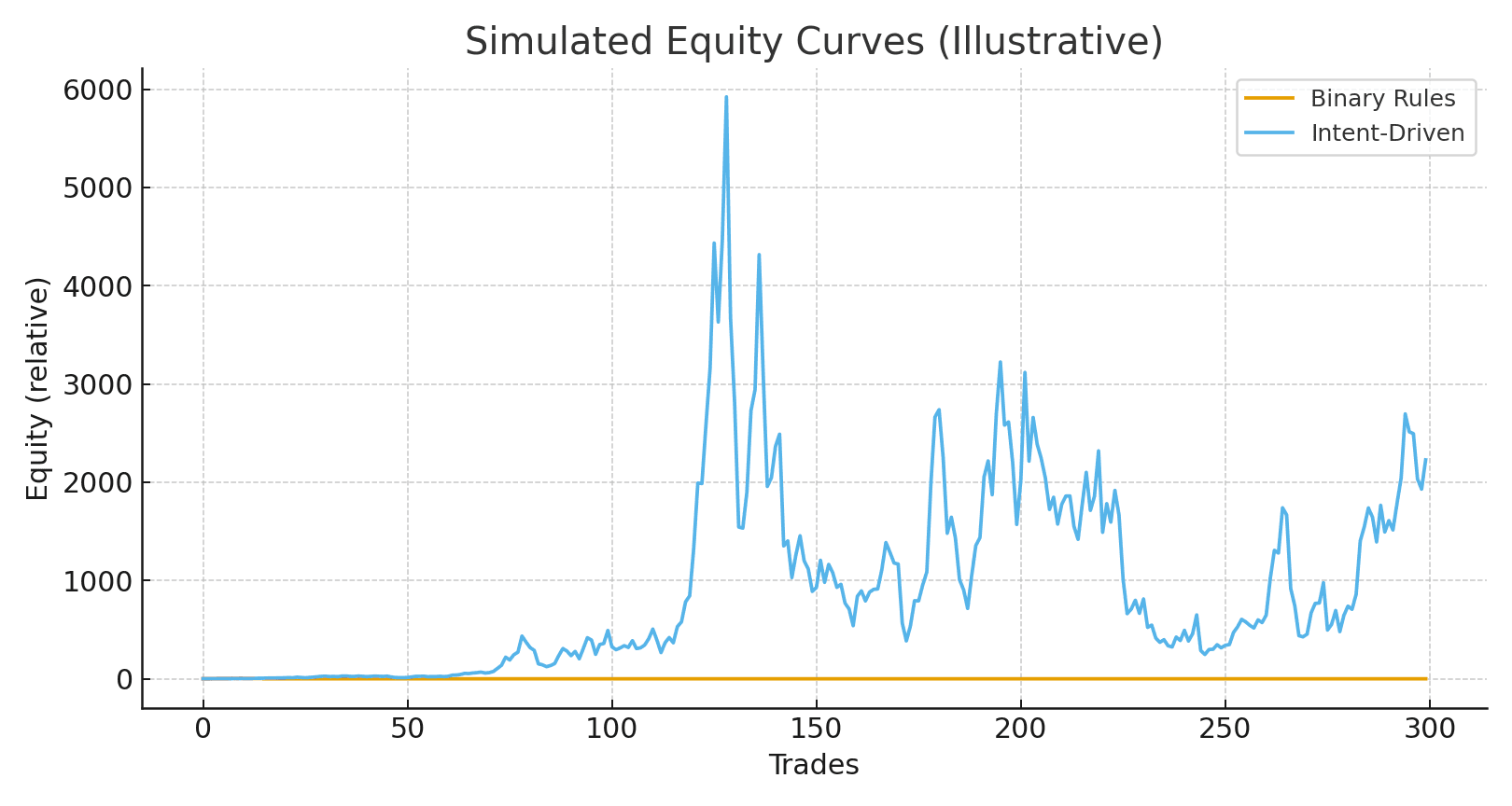

In short, binary rules snap at thresholds and ignore context. Replace them with a simple, repeatable process that ties risk to confidence, uses adaptive risk guards, and delivers steadier execution across different market conditions.

Why binary rules fail in live markets

Missing context (regime, volatility, liquidity, calendar)

Brittle thresholds create cliff effects

No representation of trader intent

Learning stalls (optimize hit-rate, not expectancy)

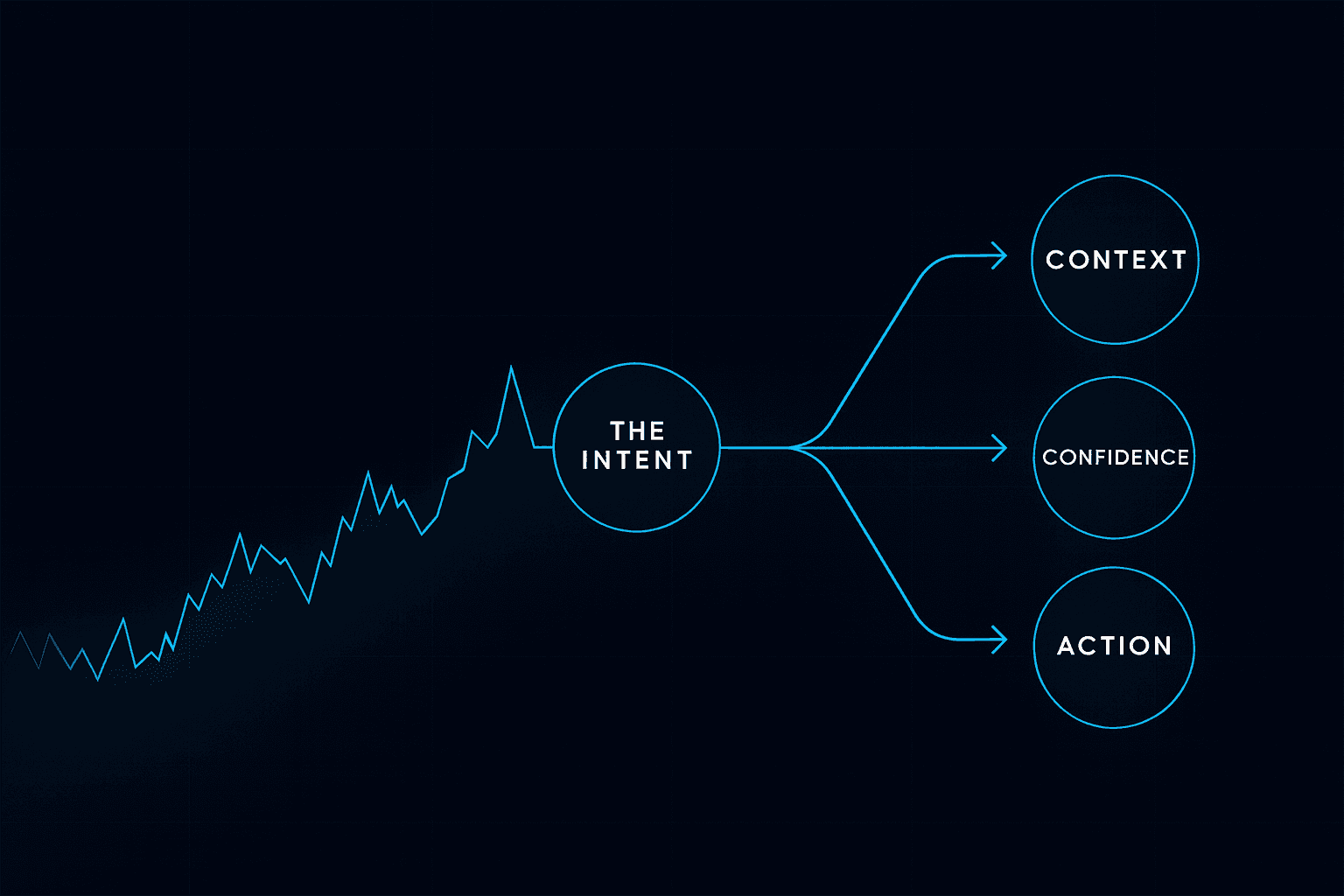

The Intent → Context → Confidence → Action model

1) Intent

One precise sentence that captures the edge in plain English. Example: “Participate when momentum pivots from support within an uptrend.”

2) Context

Regime (trend vs range, slope, persistence)

Volatility (level and percentile rank)

Liquidity (depth, spreads, impact)

Breadth / risk appetite (A/D, leadership, credit)

Calendar (earnings, macro windows)

3) Confidence

Start at 50. Add/subtract bounded weights for each context dimension (cap 0–100). The score becomes a stable bridge from messy inputs to decisions.

4) Action

Map score bands to size, entry tactics, adds/reduces, and time stops. Act proportionally (not binarily).

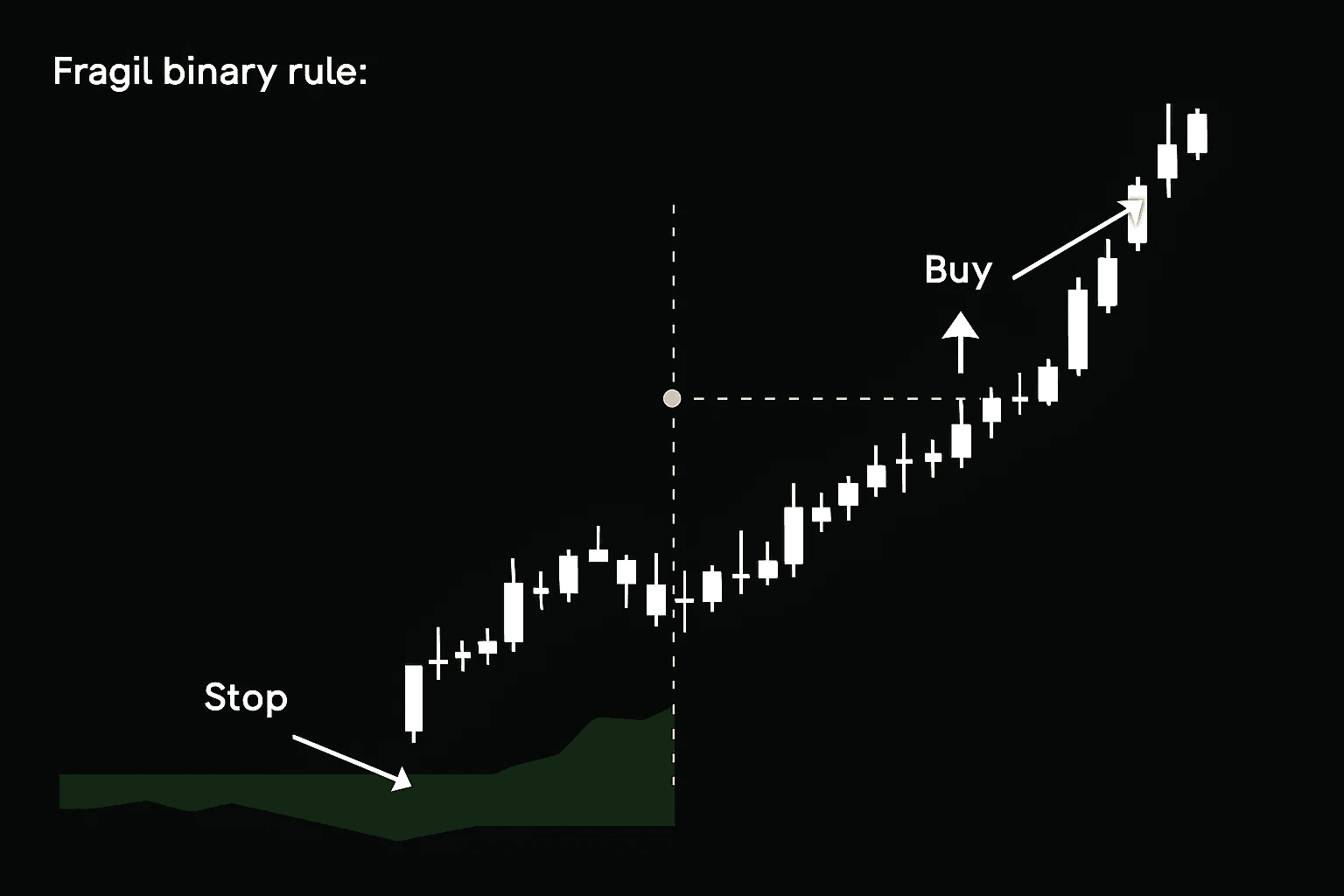

From rule to representation: a worked example

Fragile binary rule: IF price closes above a 20-day high AND RSI < 70 THEN buy; stop = 5%, target = 10%.

Adaptive representation:

Intent: Buy breakouts aligned with improving momentum and healthy internals.

Context checks: trend alignment, mid-quartile volatility, rising breadth, no events ±24h.

Confidence scoring: +10 weekly trend aligned; +10 breadth rising day & week; −10 top-quartile vol; −10 thin liquidity.

Action policy: <50 = no trade; 50–69 = starter; 70–84 = starter + add on retest; ≥85 = full allocation + time stop.

Risk envelope: ATR stop under structure; partial at 1.5R; trail remainder; portfolio drawdown guard.

Risk management as an adaptive envelope

Structural stops (behind swing structure)

Volatility normalization (ATRs, not raw points)

Time stops (exit if thesis stalls)

Portfolio guards (daily drawdown cap; compress size after stress)

Implementation steps

Write the intent (one sentence).

Pick five context checks; define how each is computed.

Score confidence (start 50; bounded ±10 weights; cap 0–100).

Create an action policy mapped to score bands.

Wrap with a risk envelope (ATR stops, structural levels, portfolio caps, news filter).

Instrument and review weekly (score distribution, expectancy by regime, policy compliance).

Case study: large-cap momentum shift

Universe: liquid large cap

Intent: participate in momentum turns from support; avoid headline landmines

Context: trend up, mid-quartile vol, rising breadth, tight spreads, no events ±24h

Policy: 60–74 = 0.5×; 75–84 = 1.0× + add on retest; 85–100 = 1.5×; time stops

Risk: 1.2× ATR stop; 2% daily drawdown cap; news gate

Review: score vs expectancy; slippage vs liquidity; compliance

What changes when you adopt this model

Decisions become proportional (size tracks conviction).

Stress drops (low-confidence states have a policy).

Learning compounds (adjust weights, not the whole system).

Execution professionalizes (nuance + discipline).

Ready to trade beyond IF–ELSE?

If your toolchain forces nuanced ideas into fragile rules, try a workflow that understands intent and adapts to context. Join our free beta and turn judgment into disciplined, measurable execution.